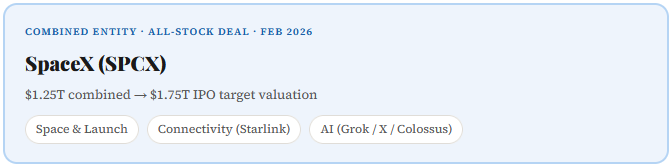

Deep Dive – Merger Analysis

The SpaceX–xAI Merger: What SPCX Investors Are Actually Buying

When you buy SPCX, you are not buying a rocket company. You are buying a rocket company, a satellite internet business, an AI lab, a social network, and the world’s largest private supercomputer — all under one ticker.

+

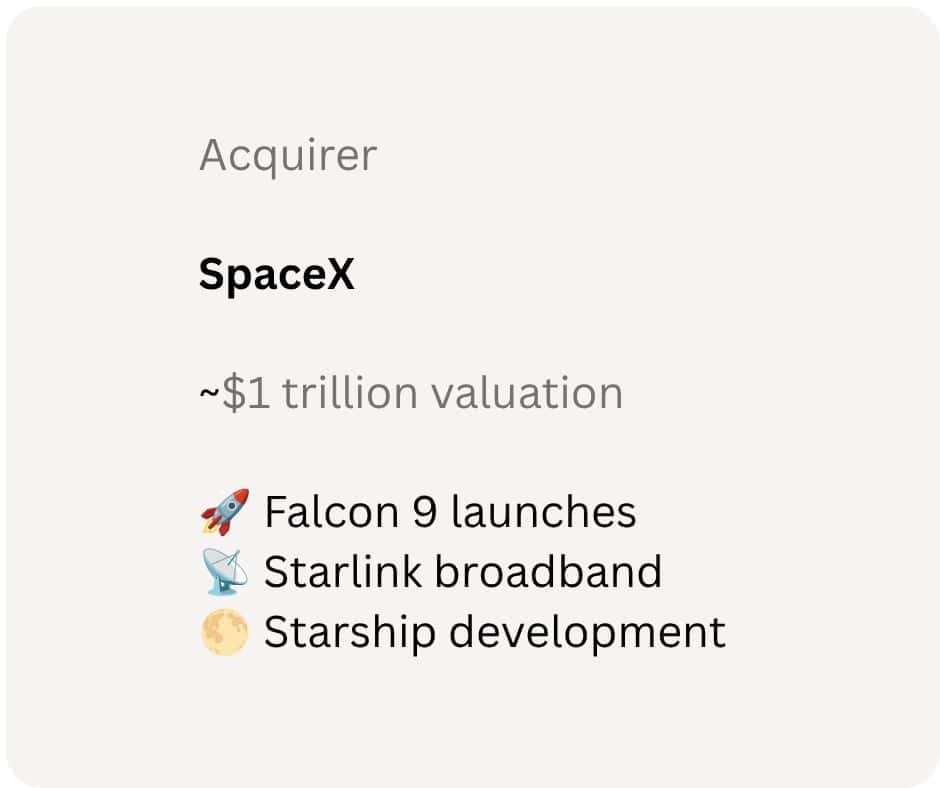

The three businesses inside SPCX

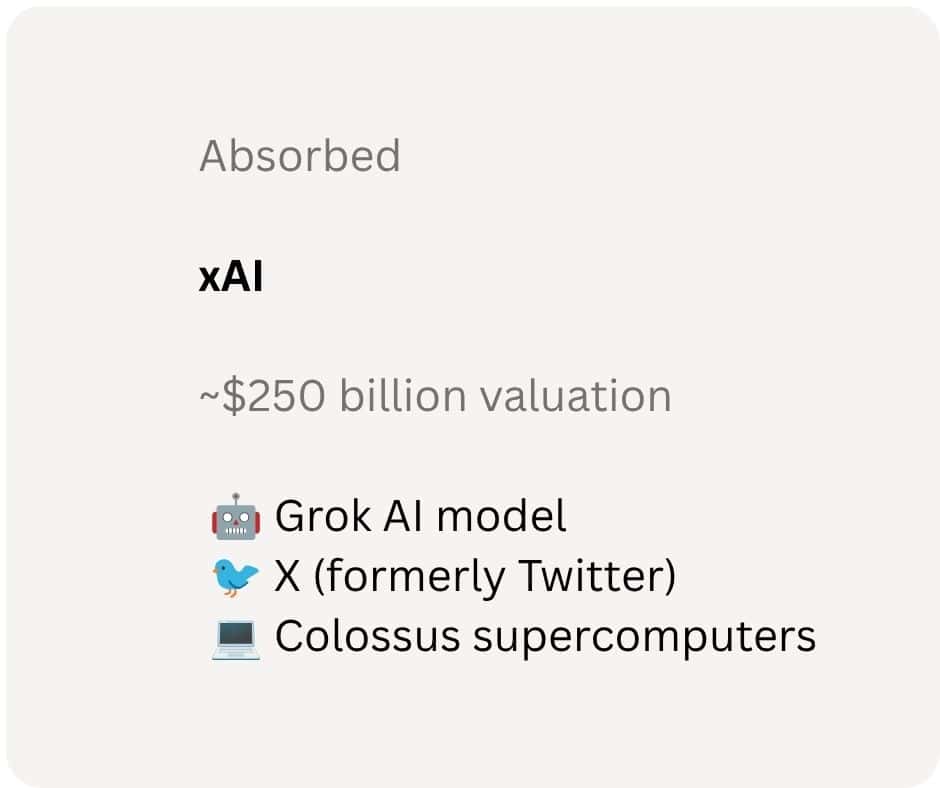

What exactly did SpaceX absorb?

Grok AI. xAI’s frontier language model, competing with GPT and Gemini. The S-1 filing reveals plans to scale Grok to “multiple trillions of parameters,” described as a “step change in reasoning.” About 117 million X users actively use Grok’s AI features.

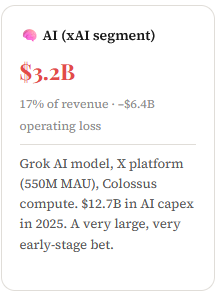

X (formerly Twitter). 550 million monthly active users. X’s real-time data stream gives Grok a training data moat that no competitor can easily replicate. The platform generates revenue through advertising and subscriptions including SuperGrok ($30/month) and SuperGrok Heavy ($300/month).

Colossus & Colossus II. Two gigawatt-scale AI supercomputer clusters in Memphis and Mississippi, built in 122 and 91 days respectively. Currently housing 555,000 GPUs, targeting 1 million. These are among the largest private AI compute clusters in the world.

Government contracts. xAI holds a $200 million ceiling DoD contract and a GSA OneGov deal making Grok available to every US federal department and agency.

Colossus GPU build-out

“The merger was not just a corporate restructuring. It was SpaceX filing its case to be valued as an AI infrastructure company — not a launch provider.”

Why did the merger happen?

In January 2026, xAI closed a $20 billion Series E — with Nvidia, Cisco, the Qatar Investment Authority, and others — at a $230 billion valuation. But xAI was burning close to $1 billion per month while generating only a fraction of that in revenue. Absorbing xAI into SpaceX solved three problems: it put xAI’s losses on a much larger, more profitable balance sheet (Starlink’s $4.4B operating income provides meaningful cover); it let SpaceX pitch investors on a higher-growth AI narrative; and it cleared the path to a single IPO rather than separate, competing listings. The deal was done entirely in stock — no cash changed hands.

What this means for SPCX investors

| Factor | Impact | Verdict |

|---|---|---|

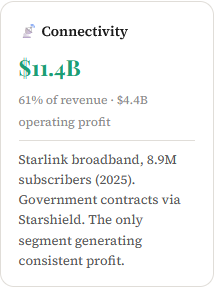

| Starlink profits now subsidise AI losses | xAI’s $6.4B operating loss is now on SpaceX’s P&L. Starlink’s $4.4B profit partially offsets it, but the combined entity is loss-making. | Negative near-term |

| AI narrative lifts the valuation ceiling | SpaceX went from $800B (Dec 2025) to $1.75T (June 2026) in under six months. The merger is the primary reason. | Positive for price |

| Colossus as a compute revenue source | In May 2026, SpaceX leased Colossus 1 capacity to Anthropic at $1.25B/month — a three-year deal. Third-party compute leasing is now a real revenue line. | Positive |

| X (Twitter) baggage included | X is losing money and carrying ~$12B in legacy debt. Every SPCX investor is also a Twitter investor, whether they want to be or not. | Negative |

| Orbital AI data centres | SpaceX plans to launch AI data centres into orbit via Starship, running on solar power. If successful, this creates a compute cost moat no ground-based rival can match. | Speculative upside |

| Grok vs. OpenAI / Anthropic | Grok currently trails on capability benchmarks and chatbot market share. The merger is a bet on infrastructure winning long-term, not current model quality. | Long-term bet |

The bottom line

The xAI merger makes SPCX simultaneously more valuable and more complex. The valuation case is now explicitly an AI infrastructure argument layered on top of the profitable satellite internet business. That is why the IPO target jumped from $800 billion to $1.75 trillion in six months — the merger is doing most of that work.

Investors must understand what they are getting: a company spending $12.7 billion a year building AI compute infrastructure, with Grok currently trailing its best-funded competitors, and with X’s social media losses sitting on the balance sheet. The Colossus–Anthropic lease deal, and the prospect of orbital AI data centres, are the clearest near-term catalysts that could justify the premium.

This analysis is for informational purposes only and does not constitute financial advice. All valuations and financials are based on publicly reported figures as of June 8, 2026.

How to Buy SpaceX (SPCX) Shares from India in 2026